Your company’s credit profile may not be something you think about every day. Yet it can influence whether your business qualifies for financing, receives favorable payment terms from suppliers, or gets approved for a commercial lease.

That makes conducting a regular business credit check an important financial habit for women business owners at every stage—not only when you’re preparing to apply for a loan.

Unfortunately, business credit can be confusing. You may wonder: Do businesses have credit scores? How can I check my business credit score? Is there a legitimate way to get a free business credit score? And what should you do when your company doesn’t have much of a credit history yet?

This guide walks you through the process step by step. You’ll learn how business credit works, where to find your reports, what information to review, and how to build company credit that supports your long-term goals.

Key Takeaways

- A business credit check shows how lenders, vendors, landlords, and other companies may evaluate your business’s financial reliability.

- Businesses can have multiple credit scores because Dun & Bradstreet, Experian, and Equifax use different data, score ranges, and risk models.

- Checking more than one business credit report can help you find missing information, reporting differences, outdated details, and potential errors.

- Establishing business credit starts with creating a separate business identity, opening accounts in the company’s name, and working with vendors or creditors that report payment activity.

- Paying bills on time, keeping balances manageable, correcting errors, and monitoring reports regularly can help strengthen your company’s credit profile over time.

Understanding Business Credit

Business credit reflects the financial history and creditworthiness of a company rather than an individual. It can help lenders, suppliers, insurers, landlords, and other organizations evaluate the likelihood that a business will meet its financial obligations.

Your business credit file may include information such as:

- Your company’s identifying details

- Payment experiences reported by vendors or creditors

- Outstanding balances

- Credit utilization

- Public records

- Collections

- Liens, judgments, or bankruptcies

- The age and size of the business

- Industry risk information

- Business credit scores and risk ratings

Not every business has a complete credit profile. A new company, for example, may not have enough reported payment activity to generate a meaningful score. Even an established company can have a thin file if its suppliers and creditors don’t report account activity to commercial credit bureaus.

That’s why checking your company’s credit profile matters. You need to know what lenders and vendors may see before you ask them to make a financial decision about your business.

Why Conduct a Business Credit Check?

A business credit check gives you an opportunity to assess your company from a creditor’s perspective.

Banks and other lenders may review business credit when deciding whether to approve a loan or line of credit. In fact, it can be a key reason why a business loan may be denied. Suppliers may use it to determine whether they’ll extend net-30, net-60, or other payment terms. A landlord might check it before approving a commercial lease.

Business credit can also affect the terms you’re offered. A stronger profile may help your company qualify for better credit limits, repayment terms, or financing costs, although approval decisions depend on many factors beyond a score.

Regular reviews can also help you:

- Detect inaccurate or outdated information

- Identify accounts you don’t recognize

- See whether vendor payments are being reported

- Understand why a credit application was denied

- Prepare before applying for financing

- Track the results of your credit-building efforts

- Notice changes that could indicate fraud or business identity theft

The Small Business Administration recommends actively establishing and managing business credit because it can help a company obtain financing and negotiate arrangements with suppliers.

Don’t wait until an urgent funding need arises. Finding an error a few days before submitting a loan application leaves little time to investigate and correct it.

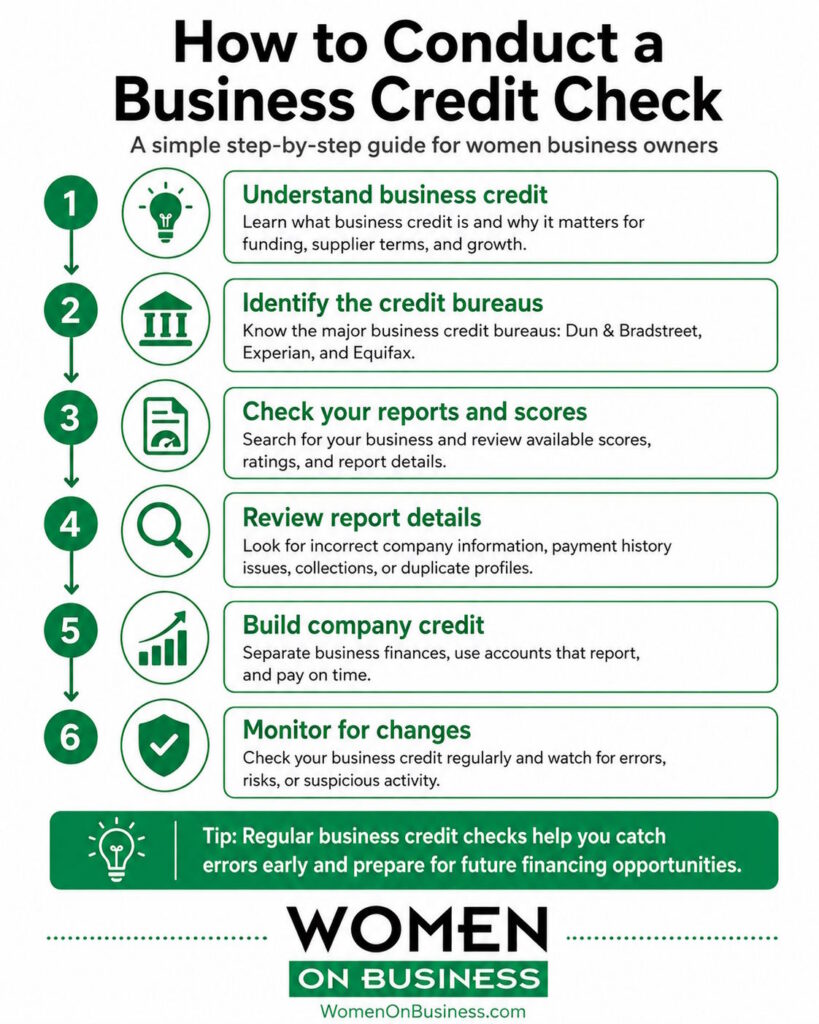

Step 1: Know the Basics of Business Credit

Before ordering reports, it helps to understand what business credit is—and what it isn’t.

Do Businesses Have Credit Scores?

Yes, businesses can have credit scores. However, business scoring is less standardized than consumer credit scoring.

There isn’t one universal business credit score that every lender uses. Commercial credit bureaus may calculate several scores and ratings, each designed to predict a different type of risk.

One score might focus heavily on past payment behavior. Another may estimate the likelihood of serious delinquency, business failure, or financial distress. The numerical ranges also vary by bureau and scoring model.

For example, Dun & Bradstreet’s PAYDEX Score ranges from 1 to 100 and is designed to reflect a company’s payment performance. Higher scores indicate a greater likelihood that the company pays its obligations on time.

A business can therefore have multiple scores at the same time. A lender may also combine commercial credit data with bank statements, revenue, cash flow, industry conditions, collateral, and the owner’s personal credit.

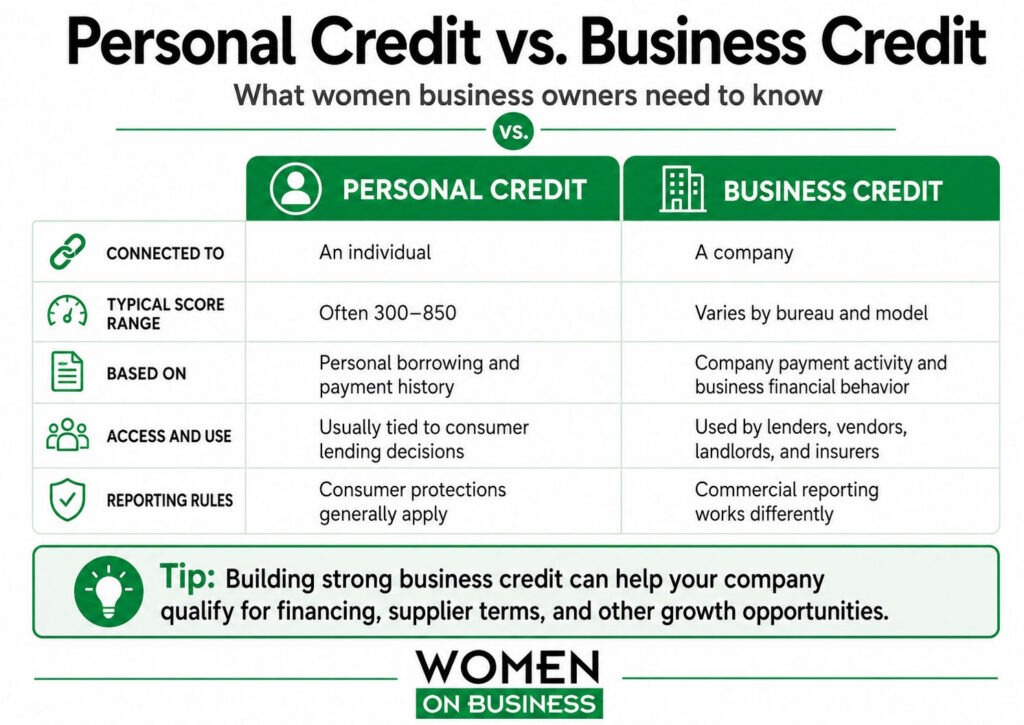

Key Differences Between Personal and Business Credit Scores

Personal and business credit both help organizations evaluate risk, but they aren’t interchangeable.

A personal credit file is associated with an individual, typically through identifying information such as a Social Security number. A business credit profile is associated with a company and may be connected to its legal name, address, Employer Identification Number, or a bureau-specific identifier such as a Dun & Bradstreet D-U-N-S Number.

Personal consumer reports are also subject to consumer protections and free-report requirements that don’t necessarily apply to commercial reports in the same way. You generally shouldn’t assume you’re entitled to free copies of all your business credit reports simply because consumers can access free personal credit reports.

Business reports may also be more broadly available for purchase. A lender, supplier, prospective business partner, or other company may be able to obtain commercial information without the same type of permission required for accessing a consumer credit report.

Finally, personal credit scores often use familiar ranges such as 300 to 850. Business scores may use ranges such as 1 to 100 or other scales, depending on the bureau and model.

Keeping business and personal finances separate can make it easier to create a distinct company credit identity. However, many small business lenders still consider the owner’s personal credit, particularly when the business is young or a personal guarantee is required.

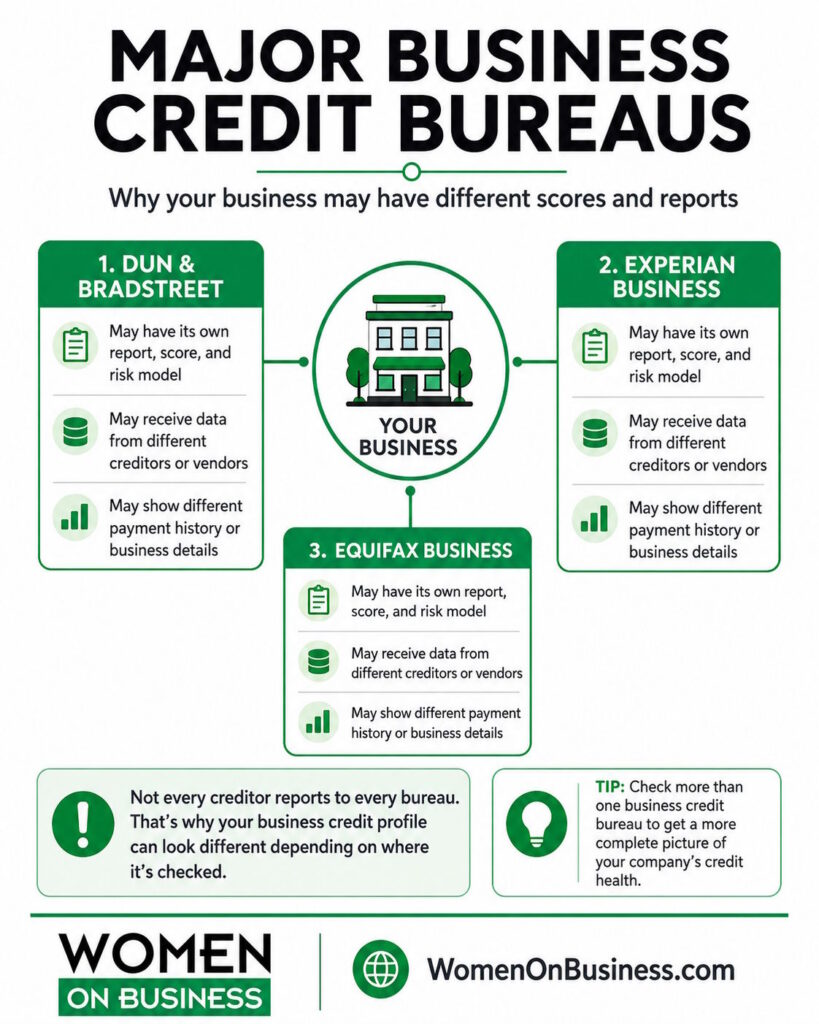

Step 2: Understand the Credit Reporting Agencies

Unlike personal credit, business credit information isn’t housed in a single centralized system. Different bureaus collect different data, use different scoring models, and may show different information about the same company.

Major Business Credit Bureaus

Three widely recognized commercial credit reporting agencies in the United States are:

Dun & Bradstreet

Dun & Bradstreet provides business credit scores, ratings, payment history information, legal-event information, and other commercial data. Its PAYDEX Score is one of its best-known measurements, but D&B business files may contain several additional scores and risk indicators.

Experian Business

Experian offers commercial credit reports, scores, monitoring, business-information updates, and dispute services. Its reports may include identifying information, payment history, account details, collections, public records, and risk scores.

Equifax Business

Equifax provides business credit reports and risk information that may be used by lenders, vendors, and other organizations. Depending on the report, information can include payment history, available credit, liabilities, and commercial risk scores.

Other specialty data providers and scoring systems also exist. In addition, some banks, fintech companies, and business-credit platforms provide scores based on bureau data or their own models.

How Do They Impact Your Business?

A credit bureau doesn’t directly approve or deny your loan. Instead, it collects and organizes information that another company may use when making a decision.

The complication is that creditors and vendors don’t all report to every bureau. One supplier might report your payments to Dun & Bradstreet, while another reports to Experian or doesn’t report commercial activity at all.

As a result, your reports can look very different.

A strong record with one bureau doesn’t guarantee that another bureau has enough data to score your company. Reviewing multiple reports can give you a more complete picture than relying on a single score.

Step 3: Learn How to Check Your Business Credit Score

To check your business credit score, start by searching for your company through each bureau’s official website.

Use your exact legal business name, location, and other identifying details. Similar company names can cause confusion, so verify that you’re looking at the correct profile before purchasing anything or submitting an update.

How Can I Check My Business Credit Score?

The basic process is usually:

- Visit a commercial credit bureau’s official website.

- Search for your company.

- Confirm the company name, location, and identifying information.

- Choose a free-access or paid-report option, when available.

- Review the scores, ratings, payment data, and company details provided.

- Repeat the process with other major bureaus.

You may need to verify that you’re an owner or authorized company representative before accessing certain details or making changes.

Be careful when using third-party websites that promise instant business credit scores. Determine which bureau supplies the data, whether you’ll receive an actual score or only a grade or risk range, how current the information is, and whether enrollment creates a paid subscription.

Free Business Credit Score Resources

Finding a genuinely free business credit score can be more difficult than obtaining a free personal credit score. Free commercial tools often provide limited information rather than a full report with every exact score.

At the time of publication, Dun & Bradstreet offers a no-cost tier of D&B Credit Insights. Its listed features include risk-range indicators for several D&B scores and ratings, basic company information, alerts, a payment-history summary, and other limited information. Exact features can change, so review the current terms before registering.

Experian provides a free company search tool that can help you determine whether your business has an Experian file. However, searching for a company isn’t necessarily the same as receiving a complete report or exact score for free.

You may also find free scores through banks, lenders, or financial-management platforms. Treat those as one source of information rather than assuming they represent every business credit bureau. Check which scoring model is being shown and when the data was last updated.

Paid Services for Detailed Reports

A paid report may make sense when you:

- Plan to apply for a significant loan or line of credit

- Want to review the information a lender is likely to see

- Need detailed payment history or public-record information

- Suspect an error

- Are evaluating another business before extending credit

- Want ongoing alerts and monitoring

Some bureaus sell one-time reports, while others offer monthly monitoring plans. Compare the information included, not only the price. A low-cost product that shows a summary score without supporting account details may not be enough to diagnose a problem.

Prices and package features can change. Review the provider’s current product description and cancellation terms before subscribing.

Step 4: Analyze Your Business Credit Report

Next, you need to analyze and interpret the data in your report.

Understanding the Report Details

Start with the basic company information:

- Is the legal business name correct?

- Are the address and phone number current?

- Is the correct industry listed?

- Are ownership or executive details accurate?

- Does the report show the right number of years in business?

- Are duplicate profiles creating fragmented information?

Next, review payment experiences and credit accounts. Look for late-payment indicators, high balances, collection accounts, and unfamiliar creditors.

Pay attention to dates. A payment listed as late might reflect a posting delay, an invoice dispute, or a creditor’s reporting error. It could also be accurate. Your job is to compare the report with invoices, bank records, account statements, and payment confirmations.

Then review public records and legal events. A lien, judgment, bankruptcy, or collection item can materially affect risk assessments. If an item belongs to another company or has been resolved but isn’t shown accurately, gather documentation.

Finally, read the explanations that accompany each score. A number without context isn’t very useful. Note the score range, what the model predicts, and the factors that may be influencing the result.

Common Errors and How to Dispute Them

Commercial credit reports can contain errors such as:

- Incorrect addresses or contact details

- Accounts belonging to another company

- Duplicate business profiles

- Payments incorrectly marked late

- Outdated balances

- Closed accounts shown as open

- Resolved legal matters shown without updates

- Incorrect industry classifications

- Inaccurate company size or revenue information

Keep a copy of the report and clearly identify every item you believe is wrong. Gather evidence, such as canceled checks, bank statements, creditor correspondence, invoices, payoff letters, or legal documents.

Follow the bureau’s official correction or dispute process. Experian, for example, provides tools for business representatives to update certain company facts and submit requests concerning report information.

Be specific. Rather than saying, “My report is wrong,” identify the creditor, account, date, reported information, correct information, and supporting document.

Keep records of everything you submit and note when the request was made. After the bureau responds, order or access an updated report to confirm whether the correction appears.

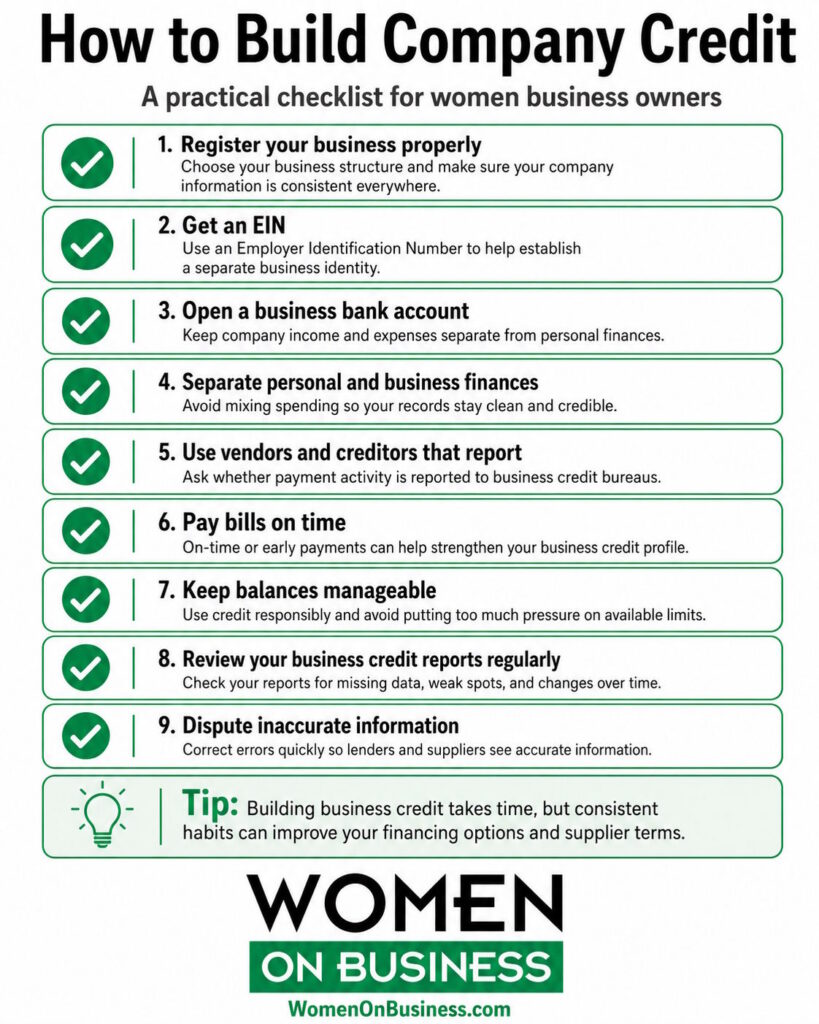

Step 5: Begin Establishing Business Credit

A business credit check may reveal that your company has little or no reportable history. That isn’t necessarily bad, especially for a new business, but it means you need to build a stronger file.

What is Establishing Business Credit?

Establishing business credit means creating a credit identity and payment history connected to your company rather than relying exclusively on your personal credit.

This process starts with presenting your business as a consistent, verifiable legal and financial entity.

That generally includes:

- Forming and registering the appropriate business entity

- Obtaining an EIN when required

- Maintaining consistent business contact information

- Opening a dedicated business bank account

- Keeping personal and business finances separate

- Creating commercial credit bureau profiles when appropriate

- Opening accounts in the company’s name

- Making payments according to the agreed terms

The SBA notes that establishing the business entity and obtaining an EIN are foundational steps toward opening a business credit file.

Formation alone, however, doesn’t create strong credit. Your company needs financial activity that is reported and evaluated.

How to Build Company Credit

Learning how to build company credit requires patience. Be wary of companies that promise a perfect score or large credit limits in a matter of days.

Start by confirming that your business information is consistent across state registrations, tax records, bank accounts, licenses, websites, directories, and credit bureau files. Small inconsistencies can make it harder to match reported activity to the correct company.

Next, ask vendors whether they report payment history to commercial credit bureaus. Opening a trade account won’t help a particular credit file if the supplier never reports it.

When applying for business credit, choose accounts your company can manage comfortably. A small limit that you use responsibly is more valuable than a large obligation that strains cash flow.

Pay every bill by the due date—and earlier when practical. Paying on time is easier when the company maintains sufficient liquidity. These strategies can help you improve your company’s working capital and reduce the risk of missing important payment deadlines. Because payment behavior can significantly influence commercial scores such as PAYDEX, a pattern of prompt payments can be an important credit-building tool.

Also manage revolving balances carefully. Avoid treating your credit limit as a spending target. High balances can signal financial pressure even when payments are technically current.

Other useful practices include:

- Keeping older accounts open when they’re affordable and still useful

- Avoiding unnecessary applications for new credit

- Maintaining adequate cash reserves

- Updating business information with the bureaus

- Correcting mistakes promptly

- Building relationships with banks and suppliers

- Reviewing whether reported activity appears on your files

Remember that strong business credit is only one piece of financial health. Lenders may still examine cash flow, profitability, debt obligations, time in business, collateral, and the owner’s personal guarantee. Maintaining accurate financial reporting is equally important because lenders rarely make decisions based on a business credit score alone.

Step 6: Monitor Your Business Credit

Business credit isn’t a task you complete once. Reports change as new payments, balances, inquiries, public records, and business details are added.

Regular Checks and Updates

How often should you conduct a business credit check?

There’s no universal schedule, but reviewing your information at least several times per year is a reasonable practice for many established companies. You may want to check more often when:

- Preparing to apply for financing

- Negotiating a commercial lease

- Seeking better supplier terms

- Making rapid changes to company debt

- Correcting disputed information

- Experiencing suspected fraud

- Planning a major expansion

- Working to improve a weak credit profile

Experian recommends monitoring business credit in advance of applying for a small business loan or line of credit so owners have time to identify problems and make improvements.

Create a simple recurring calendar reminder. Review company identifiers, payment data, account balances, risk factors, and public records. Save dated copies when possible so you can compare changes over time.

Tools for Ongoing Monitoring

Credit bureaus and third-party financial platforms offer monitoring tools that may provide:

- Notifications when scores or ratings change

- Alerts about new inquiries

- Changes to public records

- Updates to payment experiences

- Signs of new or suspicious accounts

- Periodic score access

- Recommendations based on reported risk factors

Choose a tool based on the data you need. Monitoring one bureau doesn’t necessarily reveal changes at another bureau.

You may not need a paid monthly plan forever. A temporary subscription could be useful while preparing for financing or resolving a dispute. On the other hand, a growing business that depends heavily on commercial credit may benefit from continuous monitoring.

Before enrolling, review the price, billing frequency, cancellation process, score model, bureau source, alert frequency, and level of report detail.

Frequently Asked Questions About Business Credit Checks

Do businesses have credit scores?

Yes. Businesses can have multiple credit scores and risk ratings based on payment history, balances, public records, company age, and reported credit activity. Dun & Bradstreet, Experian, and Equifax use different data and scoring models, so your company’s scores may vary by bureau.

How do you check your business credit score?

Search for your company through the official websites of Dun & Bradstreet, Experian Business, and Equifax Business. Confirm that the profile matches your legal business name and address, then review the available scores, ratings, payment history, and report details. Some information may be free, while complete reports may require payment.

How can I check my business credit score for free?

Free resources may provide a score range, summary, or basic company profile rather than a complete business credit report. Check which bureau supplies the data, which scoring model is used, and whether the service enrolls you in a paid subscription.

How can I build company credit?

Register the business properly, obtain an EIN when appropriate, open a dedicated business bank account, and keep business and personal finances separate. Use vendors and creditors that report commercial payment activity, pay bills on time, keep balances manageable, and correct report errors promptly.

How often should I conduct a business credit check?

Review your business credit reports at least several times per year and before applying for financing, negotiating supplier terms, or signing a commercial lease. More frequent monitoring may be helpful while disputing an error, building credit, or watching for possible fraud.

Make Business Credit Part of Your Financial Routine

A business credit check helps you understand how lenders, vendors, and potential partners may view your company. It can uncover errors, highlight weaknesses, reveal signs of fraud, and show whether your efforts to establish credit are working.

Begin by searching for your company with the major commercial credit bureaus. Confirm that each profile belongs to your business, review the underlying details—not only the headline score—and dispute inaccurate information with supporting documentation.

If your file is thin, focus on the fundamentals of establishing business credit. Create a consistent business identity, separate company and personal finances, work with creditors that report commercial payment activity, keep balances manageable, and pay every obligation as agreed.

Your company’s credit profile won’t determine its future by itself. Still, maintaining accurate reports and responsible financial habits can give your business more options when it’s time to borrow, negotiate, invest, or grow.