A paycheck stops when a woman retires. The consequences of decades of unequal pay don’t.

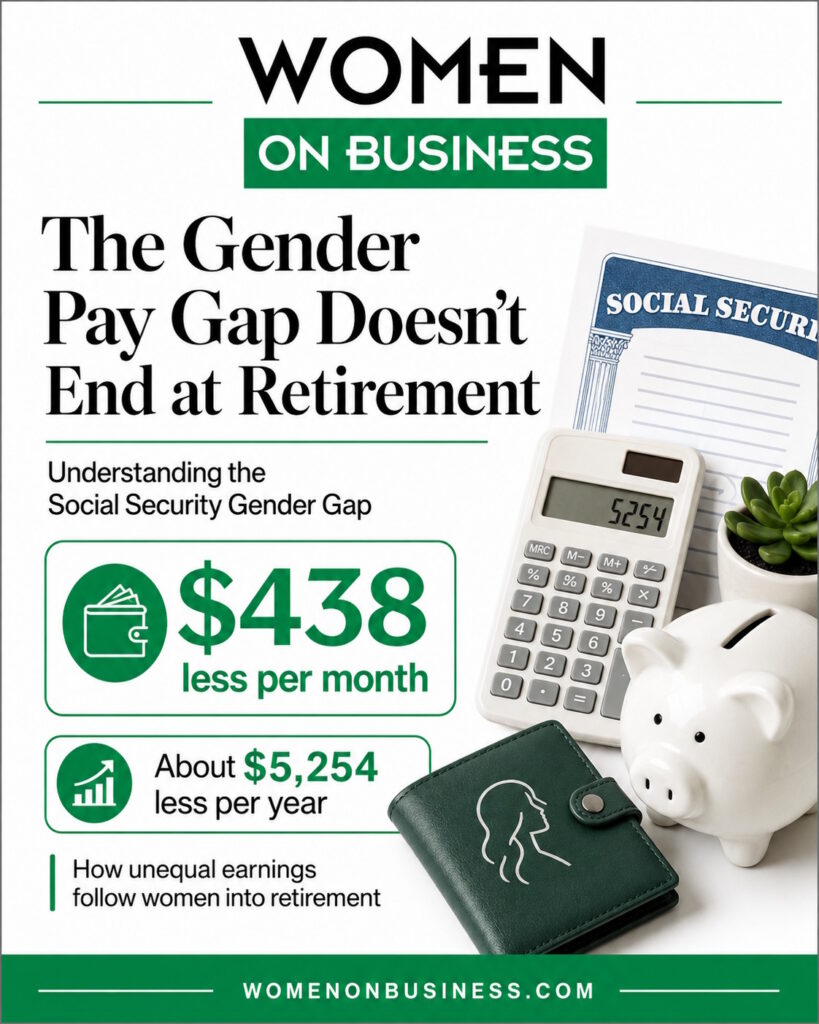

New research from FinanceBuzz reveals that women receive an average of $1,760 per month in Social Security benefits, while men receive $2,198. That’s a difference of $438 every month—or more than $5,250 over the course of a year.

For a retiree managing housing costs, food, utilities, healthcare, and other necessities on a fixed income, $438 isn’t an abstract statistic. It could cover a utility bill and groceries. It could help pay for medication. It could determine whether an unexpected home repair is manageable or financially destabilizing.

The Social Security gender gap shouldn’t be viewed only as a retirement issue. It is one, but the problem begins much earlier. It’s the cumulative result of the gender pay gap, career interruptions, caregiving responsibilities, part-time employment, occupational segregation, and unequal access to advancement throughout women’s working lives.

In other words, women don’t leave the gender pay gap behind when they retire. They take it with them.

Key Takeaways

- Women receive approximately 19.9% less in average monthly Social Security benefits than men, according to FinanceBuzz’s analysis.

- The national difference averages $438 per month and $5,254 per year.

- Social Security benefits are calculated using a worker’s highest 35 years of earnings, so lower pay and years without earnings can reduce benefits long after a woman leaves the workforce.

- Career interruptions for childcare and family caregiving can affect current income, career advancement, retirement savings, and future Social Security benefits.

- Employers can help reduce the long-term gap through equitable pay, transparent advancement practices, retirement benefits, flexible work arrangements, and support for caregivers.

- Women should treat salary negotiations, promotions, retirement contributions, and Social Security planning as connected parts of their long-term financial security.

What Is the Social Security Gender Gap?

The Social Security gender gap is the difference between the average Social Security benefits received by men and women during retirement.

According to the FinanceBuzz 2026 analysis of Social Security benefits by gender, women make up 55.1% of Social Security recipients in the United States. Despite representing the majority of recipients, women receive substantially less per person.

Using the most recent available U.S. Census Data (December 2024), the average benefits reported nationally were:

|

Recipient group |

Average monthly benefit |

Average annual benefit |

|

Men |

$2,198 |

$26,376 |

|

Women |

$1,760 |

$21,120 |

|

Difference |

$438 |

$5,256* |

*The FinanceBuzz analysis reports an annual difference of $5,254 due to calculations based on unrounded underlying figures.

The size of the gap also varies significantly by location.

Utah had the widest percentage gap in the study. Men received an average of $2,400 per month, compared with $1,751 for women—a difference of $649 per month and approximately $7,785 per year.

Washington, D.C., had the narrowest gap at 8.4%. Even there, women received an average of $174 less per month.

Geography clearly matters, but no state included in the analysis had complete equality.

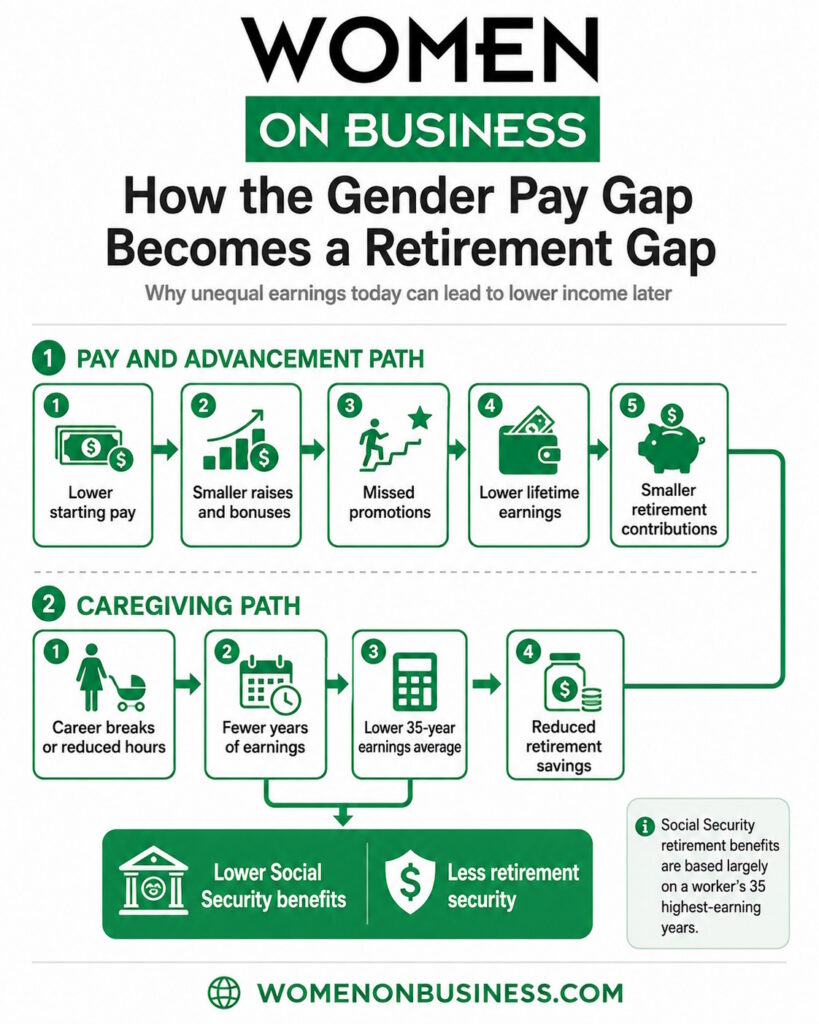

Why the Gender Pay Gap Becomes a Retirement Gap

Social Security benefits aren’t negotiated at retirement. They’re based largely on a person’s earnings history.

The Social Security Administration calculates retirement benefits using a worker’s 35 highest-earning years. When someone has fewer than 35 years of covered earnings, years without earnings can be included as zeros.

That formula may be gender-neutral on paper. The working lives feeding numbers into it are not.

Women’s median earnings for full-time, year-round work remain below men’s. The U.S. Census Bureau reported that the female-to-male earnings ratio for full-time, year-round workers was 80.9% in 2024.

One lower paycheck may not seem capable of reshaping a retirement. But lower earnings rarely happen only once. A smaller salary can lead to smaller raises, smaller bonuses, lower employer retirement contributions and less money available for personal savings.

Over 30 or 40 years, the difference compounds.

As discussed in The Longer a Woman’s Career, the Greater the Gender Pay Gap, earnings disparities can widen as women move through their careers. What begins as a relatively modest difference in pay may become much larger as raises, promotions and leadership opportunities accumulate unevenly.

Social Security eventually reflects that history.

Career Mobility Matters as Much as Starting Pay

The retirement gap isn’t caused only by two people receiving different salaries for similar jobs. It’s also shaped by who gets promoted, who receives high-visibility assignments and who reaches senior positions with substantially greater earning potential.

Women remain less likely to experience the same upward career mobility as men. They may enter an organization at a similar level but advance more slowly, encounter a broken rung early in the promotion process, or be excluded from the relationships and assignments that lead to leadership roles.

The career mobility gap for women has a lasting financial cost. A missed promotion affects more than the salary attached to one position. It may reduce every future percentage-based raise, bonus, retirement contribution and Social Security-covered earning year that follows.

A woman who misses a promotion at 35 may still be paying for it at 75.

Caregiving Leaves a Financial Record

Many women step away from paid employment, reduce their hours, or move into more flexible but lower-paying work to care for children, aging parents, spouses, or other family members.

Those decisions are often described as personal choices, but that language can obscure the reality. The truth is families frequently make those decisions not by choice but because they’re trapped in systems where paid care is unaffordable, parental leave is limited, workplace flexibility is uneven, and women are still expected to absorb more unpaid caregiving work.

The financial effects can include:

- Lost earnings during time away from work

- Smaller or missed salary increases

- Delayed promotions

- Reduced employer retirement contributions

- Lower personal retirement savings

- Fewer years of Social Security-covered earnings

The Government Accountability Office has reported that women face particular retirement challenges because they generally live longer, have lower lifetime earnings, and are more likely to serve as primary caregivers.

Research on parental and spousal caregivers has also found significant differences in retirement assets. Older spousal caregivers in one GAO analysis had an estimated 50% less in individual retirement account assets and 11% less in Social Security income than comparable married non-caregivers.

This doesn’t mean women shouldn’t take time away from work. It means caregiving has economic value, yet the systems used to calculate wages and retirement income often treat that labor as if it never happened.

What Working Women Can Do Now

No woman can personally solve a structural pay problem. Still, understanding how present-day career decisions influence retirement can help women make more informed choices.

Review your Social Security earnings record

Create or sign in to your account at SSA.gov and review your earnings history. An error in your record could affect your estimated benefits.

Pay close attention to missing earnings or years that don’t match your records.

Calculate the long-term value of compensation

When considering a position, raise, promotion, or employment break, look beyond immediate take-home pay.

Salary influences future raises, bonuses, employer retirement contributions and Social Security benefits. A difference that seems manageable today may become much larger over time.

Negotiate earlier—and more than once

Negotiation shouldn’t be reserved for accepting a new job. Women can negotiate during performance reviews, promotions, role expansions, and major increases in responsibility.

A salary adjustment secured earlier in a career has more time to influence future earnings and retirement contributions.

Protect retirement savings during career transitions

When possible, consider how parental leave, caregiving, part-time employment, self-employment, or a career break will affect retirement contributions and Social Security earnings.

A financial professional can help evaluate options, particularly when a household has to decide whose career or retirement savings will absorb the cost of caregiving.

Understand Social Security claiming decisions

The age at which a person claims Social Security affects the monthly benefit. Benefits can begin as early as age 62, but delaying a claim can result in a larger monthly payment, up to age 70.

Waiting isn’t the right choice for everyone. Health, employment, savings, debt, marital status and life expectancy all matter. The important thing is to make the decision based on an individual financial analysis rather than assuming everyone should claim at the same age.

What Employers and Business Leaders Can Do

Women shouldn’t be expected to negotiate their way out of systemic inequality one salary conversation at a time.

Employers influence the Social Security gender gap because they influence the earnings histories that benefits are based on. Business leaders can take meaningful action by:

- Conducting regular pay-equity audits

- Publishing salary ranges

- Establishing consistent promotion criteria

- Reviewing raises and bonuses for gender disparities

- Providing paid parental and caregiver leave

- Offering flexible work without penalizing advancement

- Extending retirement benefits to part-time employees when possible

- Making employer retirement contributions during paid leave

- Creating pathways for employees returning from career breaks

- Ensuring women receive revenue-generating and leadership-track assignments

It’s worth remembering that the United States enacted the Equal Pay Act in 1963. Sadly, the existence of a law doesn’t automatically eliminate the workplace structures, decisions and biases that sustain unequal outcomes.

More than six decades later, those outcomes can still be seen in women’s retirement income.

The Social Security Gender Gap Is a Business Issue

It’s easy to treat retirement inequality as a problem for older women. That framing lets employers ignore everything that happens before retirement.

Today’s Social Security gaps are the delayed results of yesterday’s compensation, scheduling, promotion, and caregiving policies.

The employee who is passed over for a promotion, denied flexibility, pushed into part-time work, or paid less than a colleague may carry the cost of that decision for the rest of her life.

Bottom-line, closing the Social Security gender gap requires more than teaching women how to save. It requires building workplaces where women have equitable opportunities to earn, advance, and remain connected to the workforce throughout their careers.

Frequently Asked Questions About the Social Security Gender Gap

What is the Social Security gender gap?

The Social Security gender gap is the difference between the average benefits received by male and female beneficiaries. FinanceBuzz found that women receive an average of $1,760 per month, compared with $2,198 for men.

How much less do women receive in Social Security?

Based on the FinanceBuzz analysis of U.S. Census Bureau data, women receive an average of $438 less per month, or approximately $5,254 less per year. The amount varies considerably by state and individual earnings history.

Why do women receive lower Social Security benefits?

Social Security retirement benefits are based primarily on a worker’s highest 35 years of earnings. Women’s lower lifetime pay due to the gender pay gap, career interruptions, part-time employment, and concentration in lower-paid occupations can produce lower benefit amounts.

How does caregiving affect Social Security benefits?

Leaving work or reducing paid hours for caregiving can lower annual earnings. When those years fall within the 35 years used to calculate benefits, they can reduce a worker’s eventual monthly payment.

Which state has the largest Social Security gender gap?

FinanceBuzz found that Utah had the largest percentage gap. Women in Utah received an average of $649 less per month than men.

Which state has the smallest gap?

Washington, D.C., had the smallest gap in the analysis at 8.4%, representing an average difference of $174 per month.

The Gender Pay Gap Follows Women Into Retirement

The Social Security gender gap shows what happens when workplace inequality is allowed to compound for decades.

It appears in a monthly benefit statement, but its origins are found in starting salaries, missed promotions, unpaid caregiving, part-time jobs, occupational segregation, and retirement contributions that were never made.

For women, the message isn’t that they’ve failed to save enough or plan well enough. The data tells a more complicated story. Women have been earning, advancing, and caregiving within systems that frequently place a lower financial value on their work.

Businesses have an opportunity—and an obligation—to change that story before another generation reaches retirement carrying the same gap.

References

- “Women Lose $5,000 Each Year to the Social Security Gender Gap—Here’s How Every State Compares.” Updated June 25, 2026.

https://financebuzz.com/social-security-gender-gap-in-each-state - Social Security Administration. “Fast Facts & Figures About Social Security, 2025.”

https://www.ssa.gov/policy/docs/chartbooks/fast_facts/2025/fast_facts25.html - Social Security Administration. “Social Security Retirement Benefits and Private Annuities: A Comparative Analysis.”

https://www.ssa.gov/policy/docs/issuepapers/ip2017-01.html - S. Census Bureau. “Equal Pay Day: March 20, 2026.” https://www.census.gov/newsroom/stories/equal-pay-day.html

- S. Census Bureau. “Income in the United States: 2024.”

https://www.census.gov/library/publications/2025/demo/p60-286.html - S. Government Accountability Office. “Is It Harder for Women to Save for Retirement?”

https://www.gao.gov/blog/it-harder-women-save-retirement - S. Government Accountability Office. “Retirement Security: Some Parental and Spousal Caregivers Face Financial Risks.”

https://www.gao.gov/products/gao-19-382